Key Question for Business Owners

As a business owner, you know that paying yourself a salary or dividend from your corporation triggers personal tax. Is there a way to access the value you’ve built inside your company completely tax-free?

- A Special Tax-Free Account: The Capital Dividend Account (CDA) is a special account for your corporation that tracks tax-free amounts. It’s not a real bank account, but a running total that allows your company to pay you “capital dividends”, which you receive with no personal tax.

- Where Credits Come From: The two main sources that add to your CDA balance are the tax-free portion of capital gains your company makes and, most significantly, the death benefit received from a corporate-owned life insurance policy .

- The Leveraging Advantage: When you leverage a life insurance policy (like in an Immediate Financing Arrangement), you can create a “Surplus CDA Capacity.” This means the CDA credit generated can be much larger than the net cash from the policy, allowing you to extract even more of your company’s other retained earnings tax-free.

Extract cash from your private corporation tax-free

Having a private corporation in Canada (including a Medical Professional Corporation) has valuable tax advantages. Since the tax rate on active business income is low (12.2% in Ontario in 2023 on the first $500,000), business owners and incorporated professionals tend to accumulate after-tax income inside their corporations.

When you take money out of your corporation as income or shareholder dividends, you are taxed personally. The overall result is comparable to earning the income directly rather than through your corporation (called “tax integration”).

Because of the low corporate tax rates on active business income, investing inside the corporation has advantages over investing personally. There are also drawbacks. When corporate retained earnings get invested, the resulting passive investment income gets heavily taxed (50.17% in Ontario) — unless you use tax-optimized strategies like an insured retirement plan or an estate bond. There is also still tax when taking cash out of the corporation.

What’s the solution?

The Tax-Free Tunnel

Getting money out of a corporation is usually expensive—you pay personal tax on every dollar you withdraw. The Capital Dividend Account (CDA) is effectively a Tax-Free Tunnel built into the corporate tax code. It allows specific funds to bypass the personal tax system entirely. However, for most businesses, this tunnel is closed because they lack the Pass Key—a tax-free death benefit. Corporate-owned life insurance provides that key, opening the tunnel and allowing dollars to pass from your company to your family with zero tax friction.

Do you have the key to the tunnel? Review the 4 Feasibility Gates.

Page Contents

- 1 Tax rates in other provinces

- 2 Investments that receive special tax treatment

- 3 What is the Capital Dividend Account?

- 4 What gets credited to the CDA?

- 5 What is a capital dividend?

- 6 How is a capital dividend declared?

- 7 When is the best time to declare a capital dividend?

- 8 How does life insurance benefit from the CDA?

- 9 Check with your accountant

- 10 How can capital dividends from life insurance help you?

Tax rates in other provinces

Moving to another province won’t help because tax rates are comparable:

| TAX RATES (federal + provincial) | Corporate Active Business Income up to $500,000 | Corporate Active Business Income above $500,000 | Corporate Passive Investment Income | Personal Tax Rate on income above $240,716 |

| British Columbia | 11.00% | 27.00% | 50.70% | 53.50% |

| Alberta | 11.00% | 22.00% | 46.70% | 47.00% (48.00% above $341,502 of income) |

| Saskatchewan | 9.00% | 27.00% | 50.70% | 47.50% |

| Ontario | 12.20% | 26.50% | 50.17% | 53.53% |

Investments that receive special tax treatment

As an individual, some of your investments receive special tax treatment:

- Capital gains: 50% of the realized capital gains are tax-free

- Death benefit from life insurance: 100% tax-free

Private corporations get the same tax advantages. There’s a dilemma: taking money out of the corporation triggers tax. The Canada Revenue Agency (CRA) has a solution: capital dividends through a mechanism called the Capital Dividend Account (CDA).

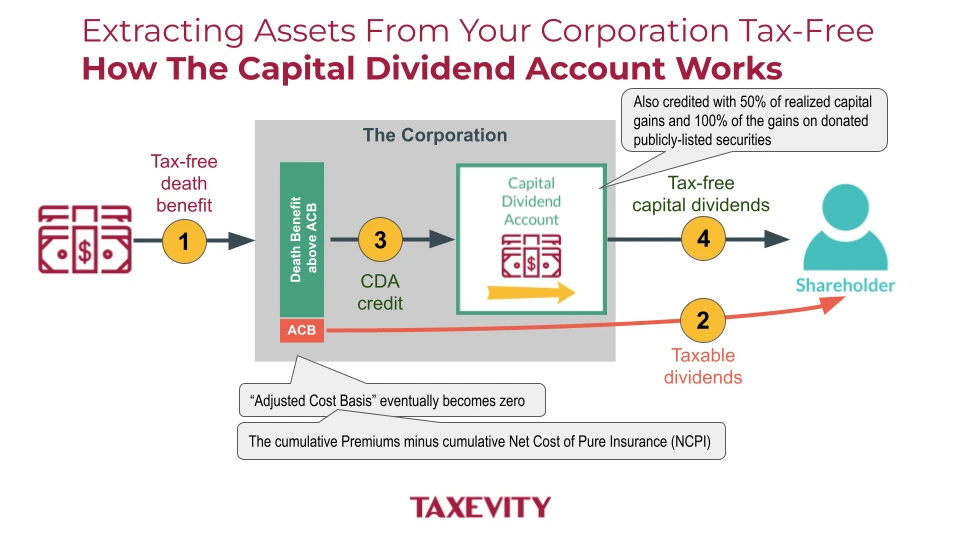

What is the Capital Dividend Account?

The Capital Dividend Account (CDA) tracks amounts that can be distributed to shareholders as tax-free capital dividends.

The CDA is notional, which means it doesn’t exist in the same way as a bank account, investment account or life insurance cash value. You will not see the CDA in your corporate financial statements, but it must be tracked. You won’t receive a formal statement showing your CDA balance. You will need to create your own. CRA Form T2SCH89 Request For Capital Dividend Account Balance Verification may help.

To file for distributions from the CDA, you must submit Form T2054 Election For A Capital Dividend Under Subsection 83(2) to the CRA before the day any part of a capital dividend becomes payable.

Not all corporations are eligible for a Capital Dividend Account. There are specific rules and calculations involved in determining the balance of the account.

Tip: To make informed decisions, consult an accountant with a deep understanding of corporate taxation. If you do not have one, we can likely make an introduction.

What gets credited to the CDA?

The Capital Dividend Account gets credited with:

- The untaxed portion of realized capital gains

- Capital Dividends received from other corporations or trusts

- Death Benefits from corporate-owned life insurance

What gets deducted from the CDA:

- The untaxed portion of realized capital losses

- The Adjusted Cost Basis from corporate-owned life insurance at the time of death

- Capital Dividends paid

Tip: Your CDA could have a negative balance because of realized capital losses. That’s why you benefit from paying capital dividends before triggering capital losses.

What is a capital dividend?

A capital dividend is a payment to shareholders that is not taxed.

Some explanations say that capital is being paid out, but this is not quite correct. A capital property triggers capital gains or losses. Life insurance does not, but death benefits above the Adjusted Cost Basis can also be paid out as capital dividends.

However, it’s important to note that:

- Not all corporations are allowed to pay out capital dividends

- Strict regulations affect when and how capital dividends can be paid

In short, a capital dividend is a way for corporations to give back to their shareholders in a tax-efficient manner.

How is a capital dividend declared?

The board of directors looks at the balance of the corporation’s Capital Dividend Account and declares how much to pay to shareholders as capital dividends.

When is the best time to declare a capital dividend?

Capital dividends are often declared once they are available. If you wait, future capital losses could reduce the balance in the CDA.

How does life insurance benefit from the CDA?

Both temporary (“term”) and permanent life insurance can use the CDA. This is one of the advantages of life insurance.

Your corporation receives the death benefit from corporately-owned life insurance tax-free. The CDA receives a credit for the death benefit minus the Adjusted Cost Basis (ACB). Since the ACB eventually becomes zero with life insurance, the entire death benefit can eventually be taken out of the corporation as tax-free capital dividends if the life insured lives long enough.

The result is that corporately-owned life insurance provides several attractive benefits:

- Premiums come from low-taxed corporate income or retained earnings.

- The corporate tax on passive investment income (50.17% in Ontario) is eliminated because investment growth is tax-sheltered inside whole life and universal life insurance (two forms of permanent life insurance).

- The cash value of the life insurance can be accessed tax-free via loans, if necessary.

- Cash from the death benefit can be taken out of the corporation as tax-free capital dividends.

Example 1: life insurance without leveraging

As an example (perhaps an estate bond), suppose:

- The death benefit is $1,200,000

- The cash value is $900,000

- The Adjusted Cost Basis (ACB) is $250,000

The CDA Credit is $950,000 ($1,200,000 – $250,000). The remaining portion of the death benefit ($250,000) can be taken out of the corporation as taxable dividends. If the life insured passes away after the ACB becomes zero, the entire death benefit could be taken out tax-free.

The cash value has no impact on the calculation (though the death benefit is always larger than the cash value).

Example 2: life insurance with leveraging

There is an additional benefit if you are leveraging your life insurance (taking loans using the cash value as collateral). This is only available with whole life and universal life insurance.

Using the figures from the prior example, suppose there is a loan of $800,000. There are two forms of insurance leveraging:

- Frontend leveraging: an Immediate Financing Arrangement (IFA) where the loan proceeds are invested

- Backend leveraging: a Corporate Insured Retirement Plan (CIRP) when the loan proceeds are spent

The net benefit after the repayment of the loan is $400,000 ($1,200,000 – $800,000).

The CDA Credit is $950,000 ($1,200,000 – $250,000). That’s $550,000 more than the net death benefit.

This means that an additional $550,000 of retained earnings can also be extracted tax-free as capital dividends ($950,000 – $400,000).

Check with your accountant

Because the Capital Dividend Account has tax implications, get guidance from an accountant who understands the taxation of private corporations.

Because tax-free capital dividends are so valuable, there are penalties for declaring a capital dividend that’s larger than the CDA balance. That’s why careful tracking and reporting is required.

How can capital dividends from life insurance help you?

Validate the Access. You have accumulated the wealth; do you have the exit strategy? Don’t let your corporate savings be trapped behind a tax wall. Whether you are planning a succession or an estate transfer, establish a rigorous standard for tax-free access.

Partner with an Architect. Book a feasibility meeting to stress-test your CDA Capacity against our engineering standards—ensuring your family gets the full value of your hard work.

See the 4 Feasibility Gates | Book a Feasibility Meeting >

At Taxevity Insurance, we’re passionate about bringing clarity to complex financial decisions. Let us empower you with personalized strategies to achieve your goals. We focus on life and health insurance solutions to protect your business, your family, and your legacy.